There are certain “lingos” in every business speech that needs to be understood before the work can be executed. These are considered terms in our everyday speech and can reflect in the financial space.

Now, what does it mean when we talk about writing off debt? Before we take you through the main focus let us dissect the concept of “to write off debt”.

When it comes to accounting, “to write off debt” means to recognise that a debt is not likely to be paid back and take it out of the books as an asset. This choice is usually made when the debtor is thought to not be able to pay back the loan.

Now that we have understood the phrase “to write off debt” let us relate it to credit score.

How certain can it be for one to write off debt without affecting credit score?

Though a debt can indeed be written off, it does not always mean the customer does not need to pay it back.

So, how can one get rid of debt without affecting his or her credit score? Does writing off debt affect one’s credit score? This and many other questions are we going to look at; in the end, you should have a fair knowledge of the process of debt write-off and its timeframe.

How can I get rid of debt without affecting my credit score?

Clearing of debt is the last thing to have on your to-do list. Getting rid of debt can be done easily but when it is associated with credit score, the consequences are quite exceptional.

Here are some guides to help you get rid of debt without compromising your credit score.

The best way to get rid of debt and keep your credit score high is to be organised and follow through with your plans.

Start by making a detailed budget that lists all of your costs in order of importance and includes money to pay off your debt. Find costs you don’t need and cut them back to get money to pay off your debt.

If you want to get lower interest rates, you might want to talk to your creditors about it. You could also look into debt consolidation, which might help you handle your bills better. Getting a consolidation loan or moving amounts with high-interest rates to credit cards with lower rates can make payments easier and save you money in the long run.

It’s best to pay off bills with higher interest rates first, even if you only have to make the minimum payments on your other debts. Set up an emergency fund so that you don’t have to use credit when you need to pay for something unexpected.

You can choose to pay off your smallest bill or the one with the highest interest rate first by using a snowball or avalanche method. This method can help you in both mental and financial ways.

Keep monitoring your credit score to make sure it is correct. If there are any mistakes, don’t be afraid to challenge them. As soon as you realise you’re having money problems, you should get in touch with your suppliers. Many of them are ready to give you short-term help or change your repayment plans to make this tough time easier.

Managing your debt in a cautious and disciplined way is important if you want to become financially free without hurting your credit score. You should also plan your finances strategically.

How long before debt is written off in South Africa?

There are so many types of debt that can be talked about. While mortgages, taxes owed, car loans, and personal loans may all be debt, their conditions are entirely different.

If you have a mortgage loan and a car loan, but you can not pay and look forward to your debt being written off, it is important to note these two are entirely different debts. Certainly, they are on your credit list, but it does not qualify them to be the same.

The time for the debt to be written off depends on the kind of debt you have found yourself in. In South Africa, the time frame for a mortgage is entirely different from minor personal loans.

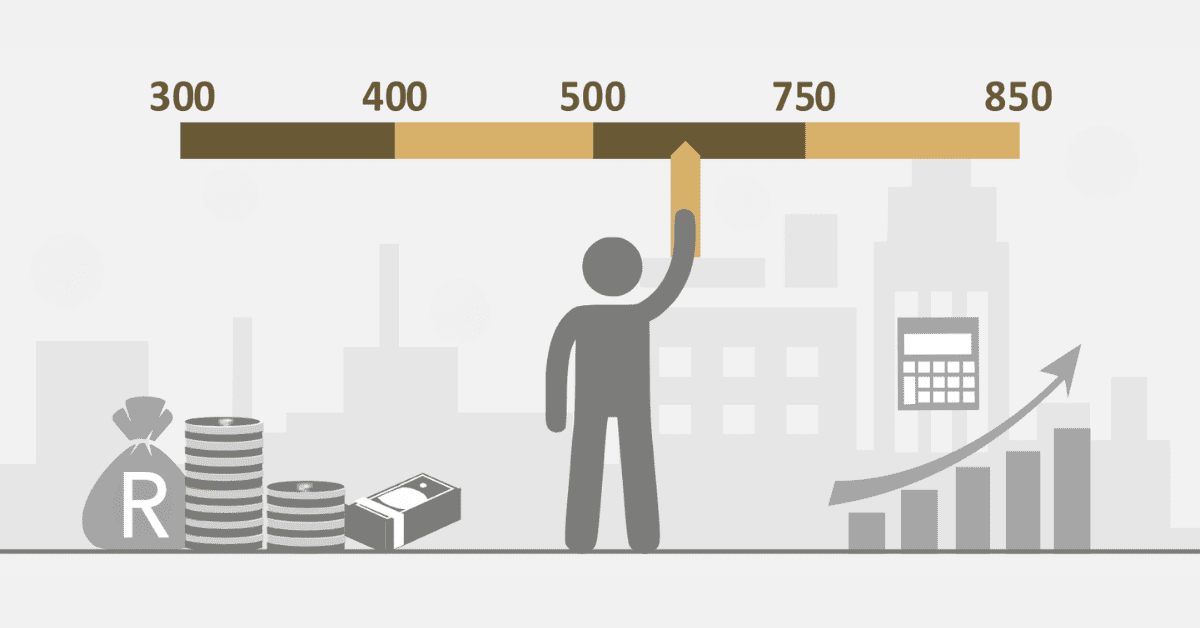

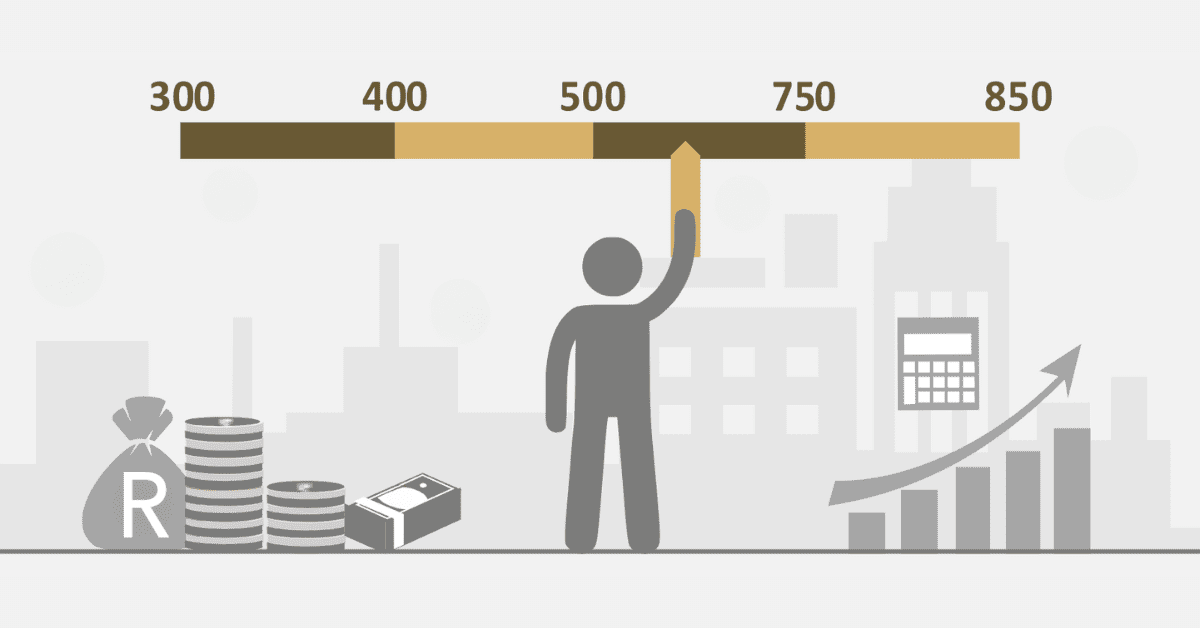

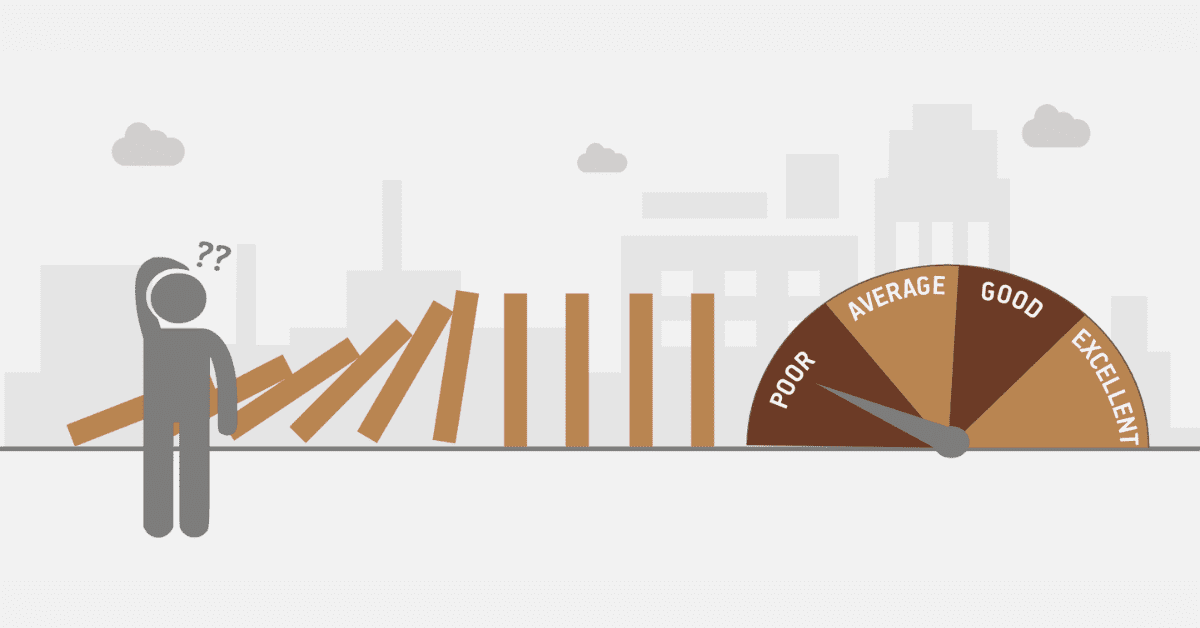

Does writing off debt affect credit score?

It is certain that writing off debt can affect your credit score. Most likely, your debt that has been written off will be recorded on your credit history and can have a negative impact on your credit history. This can disallow you to obtain a new credit for about 5 years.

How many points does credit score go up when debt is paid off?

The experts have checked and researched the number of points your credit score should gain after paying off your debt. But the real question comes in, what kind of debt and how long you have had this debt for?

Not all debts can gain you points after paying them off. Some could be less than 10, and others could be more than 5.

Ultimately, when you pay off a debt that has been around for a couple of months of an amount considered to be your minimum yearly debt, you can gain between 10 to 15 points to your credit score.