Debt is one thing that most people find challenging to handle in the complicated financial sphere. One could have debt due to many reasons, including an emergency due to a medical condition, due to a loan for one’s education, or even in the form of a credit card bill. If not managed well, it can cause stress in financial matters and tamper with the quality of life.

In South Africa, DebtBusters has taken on a pioneering role in the area of debt counselling and consolidation. With a mission to help South Africans regain control of their finances, the firm has extended a bouquet of services to enable arrear management by their clientele, which finally leads them to the land of monetary freedom. The company pledges to take a holistic approach toward debt management, ensuring that the clients are free of debt and financially educated.

How Does Debtbusters Work?

DebtBusters operates through the provision of services related to debt counselling. Upon the visit to DebtBusters by a client, they are allocated a debt counsellor who takes a broad view of their financial health, that is, analyses the client’s income expenditures and credit obligations. With this information, the counsellor can understand the fiscal health of the client and pick out the areas of concern. This is where the debt counsellor takes their cue and identifies the level of indebtedness.

For all cases in which the client is over-indebted, the client is bound to be overcommitted, and therefore, they have more monthly expenditures than monthly income, and the debt counsellor will file a court order halting further pursuit from all creditors on the client. The debt counsellor then flags the client as under debt counselling to the credit bureaus. This prevents the client from incurring even more debt-related financial stress. As a result, it enables the client to begin working on a plan to settle the debt.

Step three involves negotiating with the creditors. Here, the loan counsellor negotiates reduced interest rates and charges on the client’s credit agreements. They also negotiate to lengthen the terms of the due contracts. After all these agreements are completed, the customer has to pay only one reduced monthly instalment. This figure is distributed amongst all the creditors mentioned in the plan. This makes the procedure of repayment quite more effortless, and the customer can now easily manage the debts.

Does Debtbusters Offer Consolidation Loans?

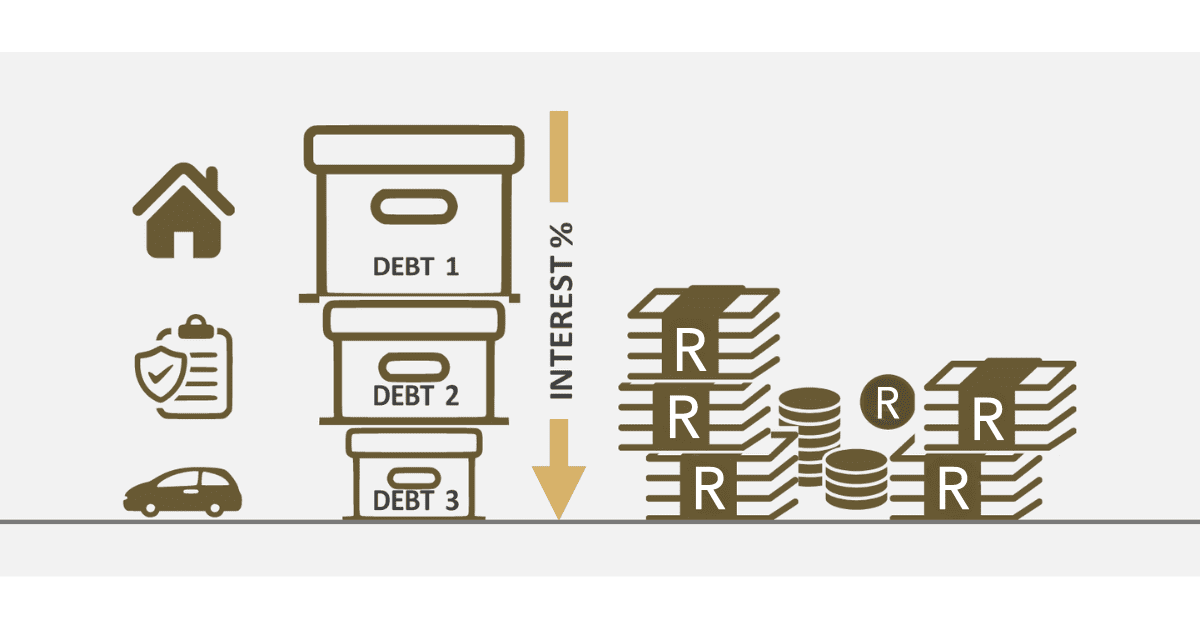

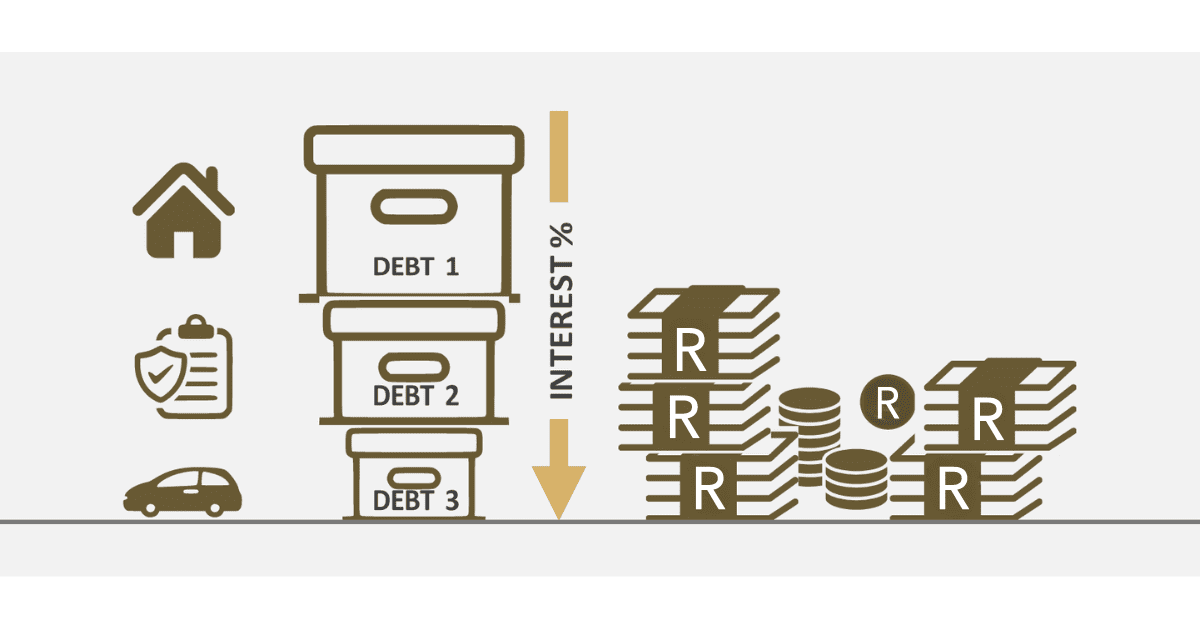

Yes, it does. Though the firm is mainly into loan counselling services, it also offers dues consolidation services. For example, with DebtBusters, however, debt consolidation comes not in the form of a loan. You will have all your debts combined into one. This eases up your financial life, and you might even. One can then focus on one payment in a month rather than juggling many payments that are due on different dates every month. What due consolidation may do is secure a better interest rate. It further reduces monthly payments. Lastly, it leads to more savings in the long run.

What Differentiates Debt Counselling from Consolidation?

These are two ways of handling arrears. However, these two have their share of advantages and disadvantages. Debt counselling is where an individual hires an expert in finance who helps in handling and budgeting the person’s credits. Haggling for reduced rates is taken care of by the arrear counsellors for a repayment plan that is affordable to the person. This process will alleviate the stress one has in dealing with many lenders. It helps you find your way back to managing and controlling your cash.

Debt consolidation, on the other hand, is borrowing a new credit to pay off existing multiple cash advances. This can simplify your arrear management by combining multiple payments into a single one. It puts you in a position where you must qualify for a new credit. Many times, this isn’t possible when your load record is horrible. Besides, though debt consolidation can be helpful in terms of making your payments much more manageable, the amount you owe isn’t reduced. You must seriously weigh your options and choose the perfect strategy according to your fiscal state.

How Do You Tell If One Qualifies For Debt Consolidation?

There are some things considered in this case. These include an average credit rating, consistent earnings, and no red flags that would make them a high-risk borrower. They will also look at the person’s debt-to-income ratio, basically the total of someone’s monthly gross earnings that goes to offset arrears.

An ideal candidate for this case would be one whose ratio is not above 50%. The thing is that every lending agency has its criteria, and what will work for one will not work for another. Therefore, it is of utmost importance to research and be sure of the requirements of every potential lender before applying for this loan.

Can I Apply For A Consolidation Loan While Under Debt Review?

While you are under debt review, you will generally not be able to apply for this credit. In general, being under this status does not appeal to the majority of creditors, as this equates to reckless lending. The rule could come with exceptions, however, and a full assessment is done to see if you would qualify for the loan. Consolidation must be done based on advice from either your debt counsellor or a financial advisor before it’s carried out under the umbrella of arrear review.

In short, DebtBusters has an extensive range of services with the aim of helping South Africans handle their debt. Whether through debt counselling or debt consolidation, DebtBusters intends to. Always remember that in managing arrears, one size does not fit all. What works for one does not necessarily function for another person. This is why it’s crucial to get to know what your fiscal situation is. Through that, you are able to look at all your options before you settle for an arrear management strategy. With a good plan and support, you will be on top of your debts and free.